Market Report A recent Colliers survey reported that the rapid growth of e-commerce established the industrial sector as the darling of commercial real estate. Industrial created a robust demand for big-box buildings in core and secondary industrial markets, expanding into new markets to reach their customer base sooner. The mass appeal of quick delivery options and a vast selection of merchandise directly correlates to the development boom for fulfillment centers as other sectors of the commercial retail real estate industry suffered store closures, plummeting demand, and rising vacancy. The U.S. will need 1 billion square feet of new industrial space this decade to keep up with demand and e-commerce sales that JLL reports will hit $1.5 trillion by 2025.

Industrial has been the top-performing asset class for several years running - and there are no indications of a slowdown. According to Cushman and Wakefield, total annualized industrial returns have averaged well over 10% since 2010, outpacing non-industrial product types.

Our Thoughts Along with multifamily, industrial assets have been the bell of the lending ball over the past year. Most of our lenders have maintained their production targets for 2021 by being highly selective. This funneling of loan dollars creates a flight of capital into industrial and multifamily which seems to be apparent in interest rates and property values.

Industrial pricing has remained consistent within the past several months. We have seen spreads from Life Co's between 135-185 bps over the 10-year US Treasury, depending on leverage, location, and borrower. Even with the treasury's recent rise, our Life Co's have still been as aggressive, if not more, than banks and credit unions.

Source: CBRE Research, Real Capital Analytics, Q4 2020.

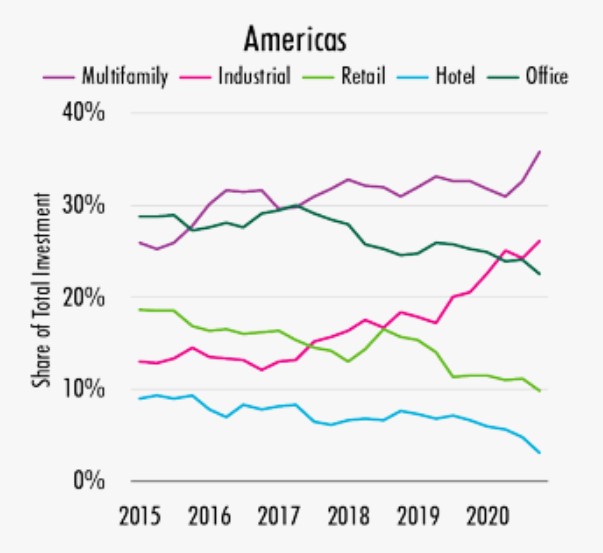

(Image above) Industrial (26%) and multifamily (36%) accounted for 62% of America's investment volume in 2020, compared with 53% in 2019.